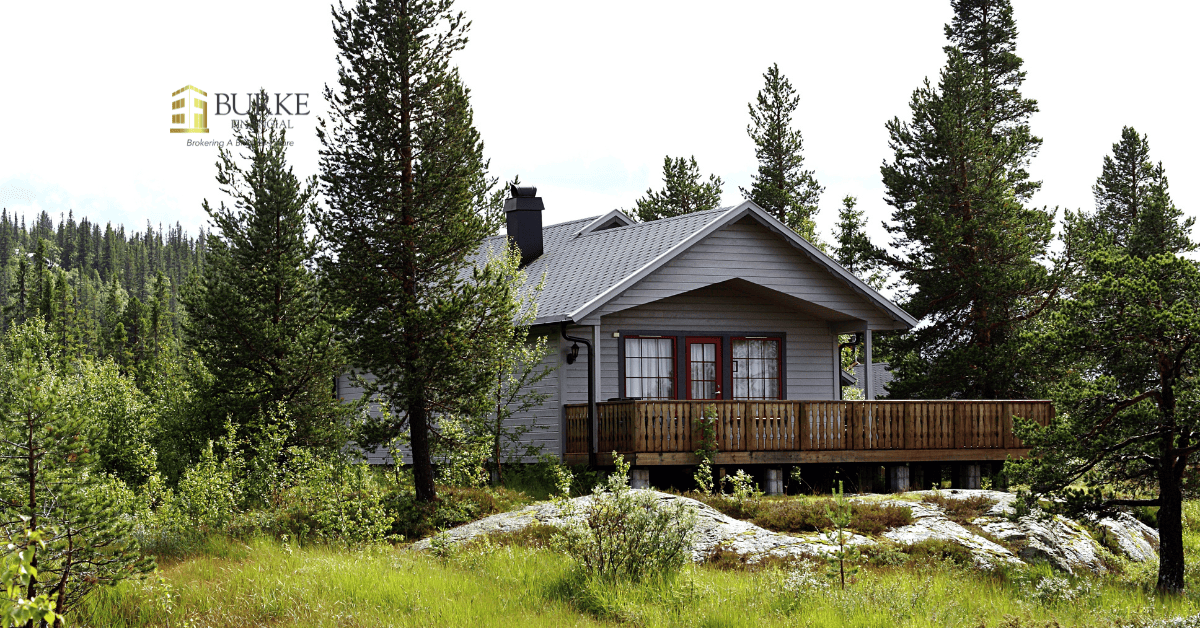

Dreaming of owning a cottage near Lake Simcoe? Whether you’re planning cozy winter escapes or summer Airbnb rentals, mortgage financing in Barrie varies based on how you’ll use the home. If you plan to use the property personally and it’s winterized, you may qualify for insured mortgage programs with as little as 10% down. But if it’s a seasonal or non-winterized property, most lenders require 20% or more equity. For investors planning to rent out on Airbnb, alternative lenders will count up to 50% of projected rental income, as long as it’s backed by a market rent appraisal. This boosts your borrowing power while keeping payments manageable. Once you have an accepted offer and appraisal, most vacation-home deals close within three weeks. Below, we’ll break down the rules by property type, explain how rental income influences your approval, and outline the hidden costs unique to Simcoe-area cottages.

Primary vs. Secondary Residence Rules

If you’re buying a vacation home that’s habitable for at least three seasons and plan to use it yourself, some insured mortgage programs may allow financing with only 10% down.

However, if the cottage is intended purely for short-term rentals or lacks key winter features like insulation and a permanent heat source, you’ll need to go the conventional route, with a minimum of 20% equity. Some lenders may even require more if the property is water-access only or lacks year-round road maintenance.

Work with a mortgage broker who understands vacation zoning, septic compliance, and municipal restrictions common to Lake Simcoe’s waterfront properties.

Financing Options & Payment Flexibility

For buyers planning to renovate or gradually transition the home into a full-time short-term rental, alternative lenders offer flexible mortgage terms. That includes:

- Interest-only periods during the first 6–12 months

- Shorter amortizations or open terms with no prepayment penalties

- More lenient debt-ratio limits, especially helpful for those carrying an existing mortgage on a primary residence

These options allow you to keep upfront payments low while investing in upgrades like HVAC, insulation, or dock repairs.

Airbnb Income & LTV Impact

One of the biggest advantages for Lake Simcoe investors is that projected Airbnb income can count toward qualification, if your lender accepts it.

Here’s how it works:

- You order a market rent appraisal from a certified appraiser

- The report estimates fair nightly or monthly rent in the area

- Your broker presents this to the lender, who will count up to 50% of that income toward the new mortgage

- This income offset reduces your debt-to-income ratio and may increase your borrowing power

This strategy is especially useful for buyers with a strong equity position but limited salaried income.

Closing Costs Unique to Lake Simcoe

Cottages and waterfront homes near Barrie come with special closing costs that don’t apply to standard residential purchases. Be prepared for:

- Septic system inspections ($400–$800)

- Shoreline road allowance reviews (especially if your lot touches public land)

- Water portability testing (required for mortgage funding if no municipal water exists)

- Property insurance for seasonal homes, which may carry higher premiums

All in, these extras can add up to 1.5% of the purchase price. Your broker can help you budget correctly and navigate lender requirements.

Want to buy a Lake Simcoe cottage with confidence?

Let Burke Financial match you with the right lender and rental-income strategy, so you can enjoy the view and protect your cash flow.

Contact Burke Financial

📞 1-866-702-9394

🌐 www.burkefinancial.ca